U.S. venture capitalists had a tremendous year in 2021, smashing all previous annual fundraising records. Total funds raised last year topped $128 billion—approximately 50% higher than the previous record of $85.8 billion raised in 2020. Venture funds invested surpassed the $300 billion mark for the first time, clocking in at $329.8 billion for the year.

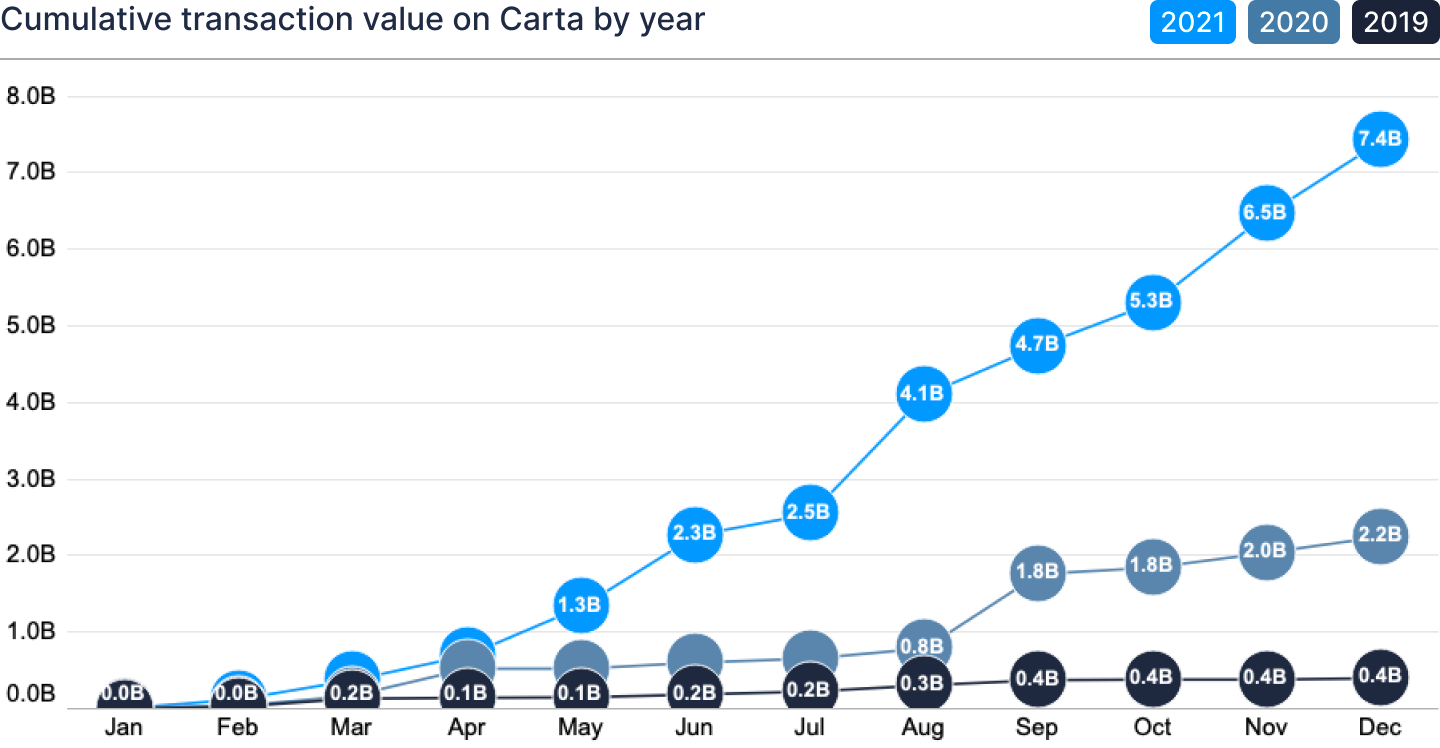

Against this background, an even stronger trend emerged: the movement toward private market liquidity. Carta completed 129 secondary liquidity transactions for private companies in 2021—more than 4x the total conducted in 2020. Dollars transacted rose from $2.2 billion in 2020 to $7.4 billion in 2021. Liquidity momentum also diversified across geographies: Companies outside California initiated 47% of secondaries on Carta in 2021, compared with just 35% in 2019.

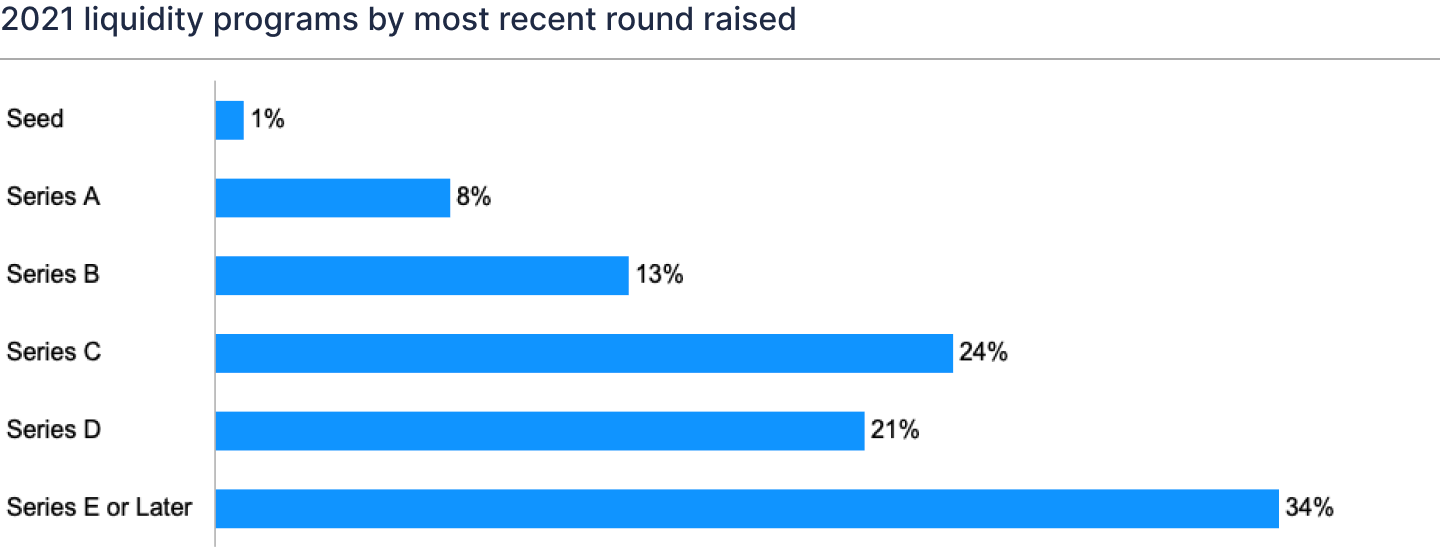

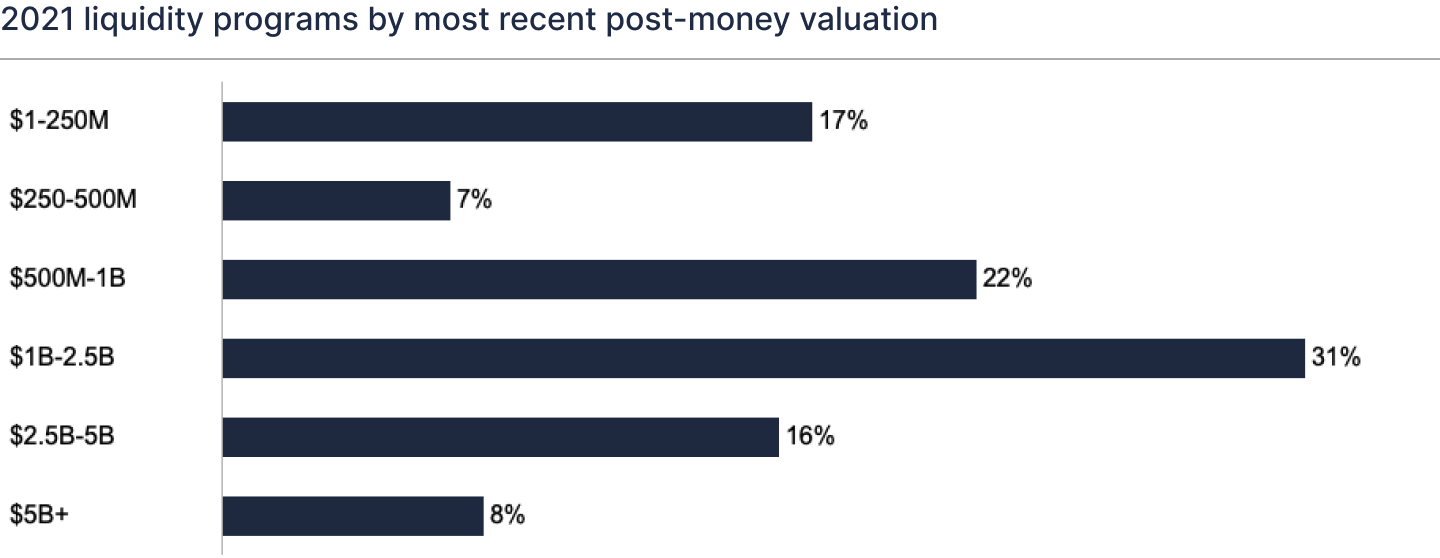

Industry observers have predicted that as the average time for VC-backed companies to exit grows, investors would turn to secondary liquidity to extract value from large, mature private companies. But Carta’s 2021 data shows that those factors are now only part of the story. Last year’s dramatic movement toward secondary transactions was distributed across private companies of all sizes and funding stages. Of companies that conducted secondary transactions on Carta in 2021, 46% were under a $1 billion valuation as of their most recent post-money valuation.

The broad-based movement toward liquidity suggests that longer timelines to IPO aren’t the only reason that companies are seeking liquidity. Secondaries also provide a way for companies to bring new investors onto their cap tables without the dilution associated with a primary round of financing. And in today’s competitive labor market—particularly in the VC-backed tech economy—secondary liquidity events can also be a way for companies to improve employee recruitment and retention by making equity compensation meaningful.

To learn more about how the movement toward liquidity has accelerated, including data analysis of liquidity transactions by geography and industry, download Carta’s 2021 liquidity report.